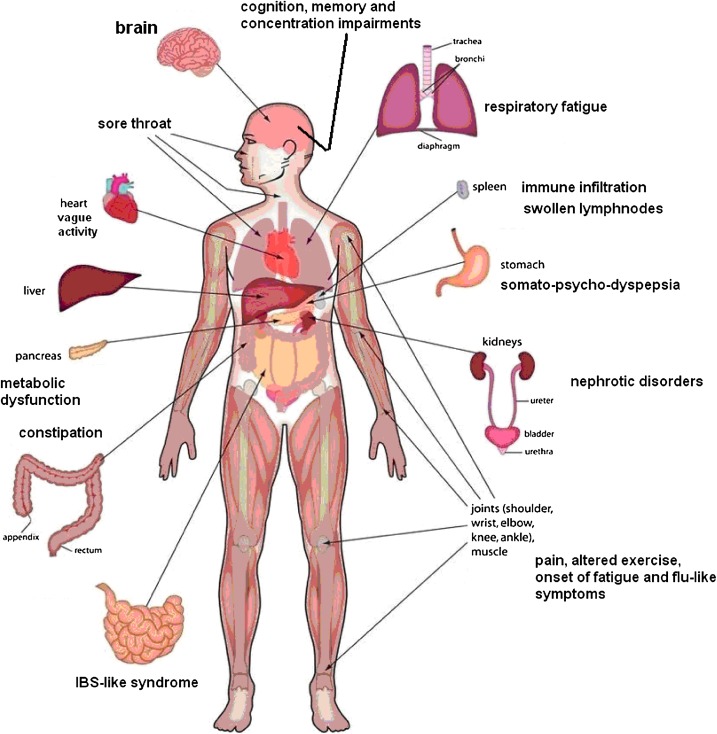

If you have chronic fatigue syndrome you know all too well that it’s far more complicated than simply feeling tired. There are a litany of symptoms that people with myalgic encephalomyelitis/chronic fatigue syndrome, (or ME/CFS), can exhibit, and they often vary in intensity and fluctuate in severity over time.

For people with ME/CFS, working can be difficult or even impossible. Fortunately, there are ways to collect long term disability benefits if you suffer with the illness.

Here’s what you need to know about how to collect long term disability benefits when dealing with chronic fatigue syndrome.

Chronic Fatigue Syndrome Can be Difficult to Diagnose

Chronic fatigue syndrome is often difficult to diagnose, as there is no specific test or screening for the condition. It’s also tied to a variety of symptoms that often come in go, symptoms that are also common with people suffering from a variety of other conditions and illnesses.

Symptoms of CFS include a variety of physical and mental issues, such as:

- Muscle pain and weakness

- Joint pain with swelling or redness

- Impairment of short-term memory

- Visual difficulties an impaired depth perception

- Problems concentrating

- Lightheadedness, dizziness, or fainting

- Labored breathing

- Disturbed sleep patterns

Because so many CFS symptoms overlap with so many other medical conditions, getting a specific ME/CFS diagnosis can be difficult. Unfortunately, in order to collect long term disability benefits for ME/CFS, you need a diagnosis.

You Might Be Able to Collect Long Term Benefits Through the Social Security Administration

Assuming that you have an ME/CFS diagnosis from your physician, you may be able to collect long term benefits through the Social Security Administration.

SSDI benefits are available to individuals that are able to meet the SSA definition of disability. To do so, you must be unable to work in any type of substantial gainful activity due to a medical condition, injury, or illness that is expected to last for at least twelve months or expected to result in death.

Because ME/CFS often renders people unable to perform their current job but able to perform others, it is very difficult to meet this definition.

Those that do meet the definition are sometimes shocked at how much (or how little) they can receive in benefits each month. In 2023, the maximum monthly SSDI benefit is just over $3,600 per month, with the average SSDI recipient collecting only $1,350 per month. SSDI benefits are also taxable, so most recipients net even less.

It’s Easier to Collect Benefits With an Individual Disability Insurance Policy

No matter what type of industry you work in, relying on SSDI benefits is not ideal. It’s better to protect your financial security with an individual disability insurance policy from a private insurance company.

With an individual disability insurance policy you decide how much you want to receive in benefits per month. The more you want to collect per month, the higher your monthly premium will be. Most insurers allow policyholders to obtain a policy that pays out up to 60% of their current income.

Individual policy premiums are paid with dollars you’ve already earned — dollars that you’ve already paid taxes on or had taxes withheld from. For that reason, the benefits you receive are not considered taxable income.

Here’s why that’s important:

Receiving benefits that equate to 60% of your salary means that you’re likely to bring home about the same net amount that you were earning when you were working.

Read this definitive guide to physician disability insurance to learn more about disability insurance for physicians and other high income earners.

Protect Yourself With the Own Occupation Definition of Disability

Every disability insurance policy has a definition of disability, which is a standard that you have to meet in order to qualify to receive benefits.

Under the SSDI definition of disability, you cannot work in any job. Some private insurance companies offer a different definition where you can collect benefits even if you are still able to perform some amount of work. This is known as the “own occupation” definition.

With an own occupation policy, you will be eligible to collect benefits as long as your ME/CFS prevents you from doing all or some of your current job.

Technically, the own occupation definition doesn’t even require you to have an official ME/CFS diagnosis. You simply have to provide medical evidence from your physician that you have certain conditions that render you unable to do the job you currently do.

For example, a surgeon with CFS symptoms of joint swelling in the hand may not be able to hold the surgical instruments required to perform surgery. Under the own occupation definition of disability, this symptom alone could make you eligible to receive benefits.

In Conclusion

Chronic fatigue syndrome can affect both your physical ability and your mental health, and when it does, working can be nearly impossible.

An ME/CFS diagnosis may qualify you to receive disability insurance benefits through SSDI, but for that to happen your condition must be severe. It’s better to protect yourself and your financial future with an individual insurance policy with an own occupation definition.

The flexible requirements of an own occupation policy make it much more likely that you’ll be eligible to receive long term benefits when you need them most.